Over the past several months, you may have heard in conversation with your advisor, or through one of our fireside chats, the concept of the Wisdom of Crowds(WOC). And while you may have been offered a brief explanation of what this concept/phenomenon is, ultimately this topic could be talked about in much greater depth, as the examples and implications of the ideas surrounding the WOC are much further reaching than what they might first seem.

The purpose of this post is to shed a bit more light on what exactly the concept surrounding the WOC is, discuss various examples of the places and spaces it can be seen throughout time and history, and in turn discuss how we’re leveraging this idea here at Verde to offer the best possible services we can to you at clients. Perhaps the best way to convey this concept to start, is to quote one of the first individuals known to have engaged with thought surrounding the WOC, Aristotle in 350 BCE:

“it is possible that the many, though not individually good men, yet when they come together may be better, not individually but collectively, than those who are so, just as public dinners to which many contribute are better than those supplied at one man’s cost.”

Put in simple terms, the wisdom of crowds acknowledges the individual and diverse experiences of each person within a group, and takes into account each person’s respective level of expertise on a particular topic in order to come to a consensus on an answer that’s better than any individual would be able to produce on their own. The idea here is that each individual’s response has bias, but when the average is taken of all responses, this goes in some way to cancel out the outliers of people who might know less than others on a particular topic.

The quintessential example of the WOC brings us to the West of England Fat Stock and Poultry Exhibition in 1906. The scientist and statistician Francis Galton asked 787 people in attendance at the exhibition, how much they individually thought a particular steer weighed. When all the individual’s responses were collected and the average was taken, the collective guess for the weight of the steer was 1,197 pounds. The actual weight of the steer? 1,1989 pounds.

This astonishing finding doesn’t stop here however. These findings of how crowds can work in tandem to deduce solutions to complex issues can also be seen in the popular television program, Who Wants to Be a Millionaire? For those unfamiliar with the show, an individual is asked a series of increasingly difficult questions, winning increasing amounts of money for each question they complete successfully. The participant also has a series of “lifelines” that allow them to ask different individuals for help on a question they may be stumped on. One of the lifelines, “Ask the Audience” allows the audience to be pulled for what their guess is on the answer to a certain question. When this particular lifeline is used, the audience is seen to be accurate in their most widely selected answer to the question, some 95% of the time.

We’ve seen how the WOC could be used to answer some arbitrary questions such as the weight of a cow, or the answer to trivia questions, but what importance does this have to decisions that hold a little more weight in the real world? We’re glad that you asked! A more serious example of this theory in practice relates to the Challenger space shuttle accident, and the stock market.

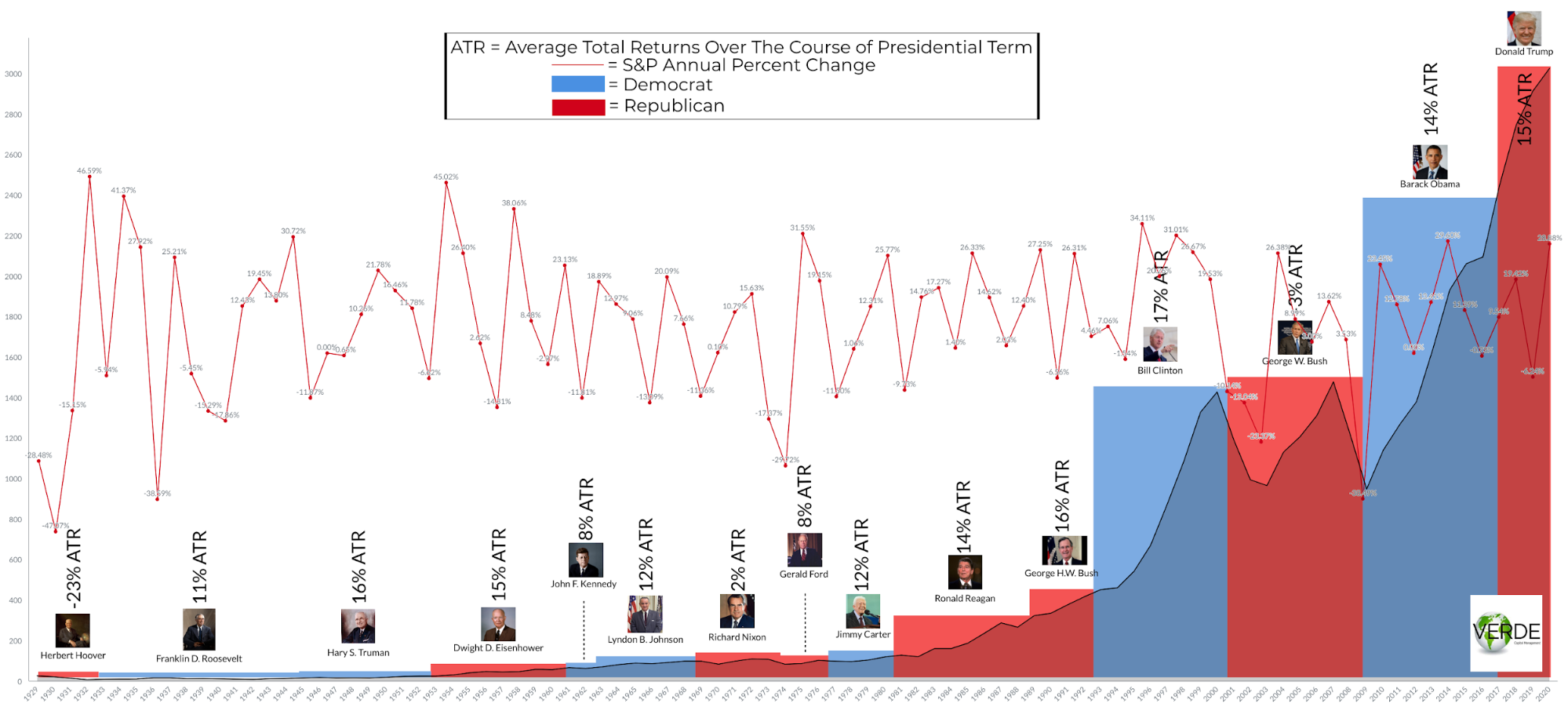

In 1968, the Challenger space shuttle was destroyed just 73 seconds after it’s launch, unfortunately leading to the fatalities of all 7 astronauts who were on board. The stock market is always responding to major changes and stories in the news, due to inventors concerns as to the profitability of certain companies that will in effect be held responsible for certain events ect. Almost immediately after the explosion, investors began selling stock of the 4 contractors involved with the launch of the challenger: Lockheed, Rockwell International, Martin Marietta, and Morton Thiokol.

By the time trading had ended for the day, Morton Thiokol’s stock had fallen by almost 12% in comparison to the 3 other companies who had only fallen by about 3% each. In other words, the stock market felt that Morton Thiokol was to blame for the disaster, however no firm evidence could be given either way as to who was to blame. 6 months later, it was found that Morton Thiokol was indeed to blame for the accident, on account for the faulty O-ring seals produced by the company.

Even in situations where there’s not a direct question being asked of a group of individuals, collective thought is at play, and can lead to some astonishing findings.

In order for the WOC to effectively and accurately be used, four different elements must be present:

- Each individual must make their guess independent of each other, and without the knowledge of what other people are guessing,

- Each individual whose response is being collected must represent a diversity of thought. The crowd should be comprised of individuals with varying levels of expertise on the particular topic at hand,

- Individuals should be able to make their guesses by drawing on their own private knowledge,

- There also must be a way to aggregate the responses form the group in order to find an ‘average’ response, which is not always the case with any possible question that you could ask a group of people.

How is Verde putting the Wisdom of Crowds into practice? Since 2015, we founded and have been utilizing our investment committee: a group of individuals within our company with diverse opinions and experiences with investment selection. Each quarter, our investment committee meets in order to discuss the selection and allocation of investments within our client’s portfolio models, by which performance is ultimately determined. It is the goal of our investment committee to make the best possible choices harnessing the wisdom and input of all group members in order to make the best decisions that benefit our clients.

It doesn’t just stop at our investment committee however, the Wisdom of Crowds has been integrated into our office culture, so as we continue to expand our team of individuals from all sorts of backgrounds, we can become stronger and more accurate decision makers.

In 1968, the US navy lost one of its submarines on the ocean floor, furthermore it seeked to find the wreckage. Unfortunately, intelligence was unable to deduce a small enough location to even look for the submarine. John Craven, a naval officer, concocted a series of scenarios by which the submarine’s location could be found. He gave a series of mathematicians, submarine specialists, and salvage men the different scenarios of where the submarine may have landed, and asked them each individually to give their best guess as to how likely their given scenario was. Craven used an aggregate theorem called Bayes’ theorem, which allowed him to calculate how new information about an event changes you pre-existing expectations of how likely an event was to occur.

When all responses from the different scenarios were aggregated, and a location was decided upon for the submarine’s likely resting place, the actual resting place of the submarine was found to be only 220 yards away from what Craven’s calculations had told him. Verde cannot predict the future of the market (as no person can), however we come together as a group of professionals with individualized specialties to help you navigate through uncertain waters.

Verde Capital Management, Inc. is a federally registered investment adviser. The information, statements and opinions expressed in this material are provided for general information only, are based on data we believe to be accurate at the time of writing, and are subject to change without notice. This material does not take into account your particular investment objectives, financial situation or needs, is not intended as a recommendation to purchase or sell any security, and is not intended as individual or specific advice. Investing involves risk and possible loss of principal capital. Diversification does not ensure a profit or protect against a loss. Past performance is not indicative of future returns. Advisory services are only offered to clients or prospective clients where Verde Capital Management, Inc. and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Verde Capital Management, Inc. unless a client service agreement is in place.