Staying ahead of shifting tax codes and new investment vehicles is key to building multi-generational wealth. One of the most talked-about legislative updates on our radar is the introduction of Trump Accounts¹.

If you are a parent or grandparent looking to give a child a financial head start, this new vehicle introduces unique planning options. Here is a high-level breakdown of how Trump Accounts work, how they stack up against legacy accounts like 529s and UTMAs, and a sophisticated Roth conversion strategy to optimize them once your child reaches adulthood.

What is a Trump Account?

A Trump Account is a tax-deferred, long-term savings vehicle designed exclusively for minors under the age of 18. The primary intent behind these accounts is to democratize investing, allowing children to build an asset base early in life.

Withdrawals are strictly prohibited while the child is a minor. Once the child turns 18, the account automatically converts into a Traditional IRA in the young adult’s name.

Key Provisions & The $1,000 Government Seed

To incentivize early adoption, the federal government introduced a pilot program offering a one-time, $1,000 Treasury contribution².

- Eligibility: The $1,000 seed money is available to U.S. citizens born between January 1, 2025, and December 31, 2028.

- The Catch: It is not automatic. A parent or guardian must explicitly elect to open the account and claim the $1,000 deposit by filing IRS Form 4547 through their online IRS account.

- Older Children: Children born before 2025 who are still under 18 can still have a Trump Account opened for them, but they do not qualify for the initial $1,000 federal deposit.

Core Mechanics of the Account

Understanding the constraints and contribution rules is essential before incorporating these into a comprehensive financial plan.

- No Earned Income Required: Unlike a traditional or Roth IRA for minors, a child does not need a W-2 or earned income to have contributions made to a Trump Account.

- Contribution Limits: Families, friends, and the child can contribute up to $5,000 per year total. (The $1,000 government seed does not count toward this annual limit).

- Corporate Matching: Employers can elect to contribute up to $2,500 per year toward the child’s account on behalf of an employee. This employer contribution is excluded from the parent’s taxable income³.

- Investment Restrictions: To keep costs low and protect less experienced investors, the law requires that Trump Accounts be invested strictly in unleveraged, broad U.S. equity index funds or ETFs (such as an S&P 500 tracker) with an expense ratio capped at 0.10%. Active trading and individual stock picking are prohibited during the child’s minority.

- Tax Treatment: Contributions are made with after-tax dollars, growth is tax-deferred, and distributions later in life are taxed as ordinary income.

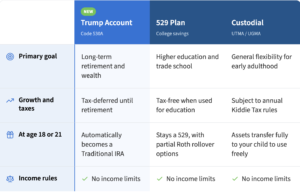

Strategic Comparison: Trump Account vs. 529 vs. UTMA

A Trump Account should not necessarily replace your current gifting strategy, but rather complement it depending on your family’s specific goals.

Who is it appropriate for?

Use a 529 plan if your primary, non-negotiable goal is funding higher education with maximum tax-free efficiency.

Use a UTMA/UGMA if you want your child to have access to funds in their early 20s for flexibility (e.g., buying a car, wedding, or travel), recognizing that they get full legal control of the money at adulthood.

Use a Trump Account if your goal is generational wealth compounding. It is highly appropriate for parents who want to lock money away strictly for the long term, preventing the child from spending it impulsively at age 18 while securing corporate matching or the $1,000 government seed.

The Advanced Play: The Young Adult Roth Conversion Strategy

Because the Trump Account converts into a Traditional IRA at age 18, all future withdrawals in retirement will be taxed as ordinary income. However, smart financial engineering allows families to turn this tax-deferred bucket into a tax-free bucket via strategic Roth conversions.

When the child turns 18 or enters early adulthood (college years or first entry-level job), they will likely be in the lowest income tax bracket of their life. This is the optimal window to execute a Roth Conversion.

How the Strategy Works:

- The Hand-off: At age 18, the Trump Account becomes a Traditional IRA owned by the child.

- Exploiting Low Income Brackets: While in college or working a part-time/low-paying entry job, the child’s standard deduction will wipe out a significant portion of their income tax liability.

- The Conversion: The young adult can convert chunks of the Traditional IRA into a Roth IRA. They will owe ordinary income tax on the amount converted, but because their income is so low, they will pay minimal or even $0 in actual taxes on that conversion.

- The Ultimate Result: Once shifted into a Roth IRA, that money will grow and be withdrawn completely tax-free in retirement.

Planning Note: Parents or grandparents can legally pay the tax bill generated by the Roth conversion on behalf of the child as a gift, ensuring the entire balance remains intact to compound inside the Roth IRA.

The Bottom Line

The Trump Account introduces a compelling new layer to minor savings strategies. For families with children born between 2025 and 2028, securing the free $1,000 Treasury seed is a financial no-brainer. From there, integrating the account alongside a 529 plan and UTMA can create a powerful, dual-track structure: funding their education today while setting up a tax-free retirement runway for tomorrow.

If you want to evaluate how a Trump Account fits into your existing estate planning or corporate benefits structure, please reach out to a Verde advisor.

¹ Source: https://uscode.house.gov/view.xhtml?req=granuleid:USC-prelim-title26-section530A&num=0&edition=prelim

² Source: https://www.whitehouse.gov/wp-content/uploads/2025/08/Trump-Accounts-Give-the-Next-Generation-a-Jump-Start-on-Saving.pdf#:~:text=Children%20born%20before%20January%201%2C%202025%2C%20who,lower%20average%20account%20balances%20for%20this%20group.

³ Source: https://www.whitehouse.gov/research/2025/08/trump-accounts-give-the-next-generation-a-jump-start-on-saving/#:~:text=Employers%20may%20make%20an%20annual%20contribution%20of,28%20if%20no%20contributions%20are%20made.%20Related

Disclosures

The information provided in this article is for educational and illustrative purposes only and does not constitute personalized investment, legal, or tax advice. Verde Capital Management (“Verde”) is a registered investment adviser. Registration does not imply a certain level of skill or training.

Past performance is no guarantee of future results. All investments involve risk, including the potential loss of principal. Tax laws are complex and subject to change. Please consult with a qualified certified public accountant (CPA), tax attorney, or your dedicated financial advisor at Verde Capital Management before executing any strategy mentioned in this article.